Tax Reform - Unrelated Business Income

by Tracy Paglia, Moss Adams: The Tax Cuts and Jobs Act (TCJA), signed by the President in late December 2017, included several provision affecting tax exempt organizations and their calculation of unrelated business income (UBI). These provisions are generally effective for the organization’s tax year beginning after December 31, 2017:

Fringe benefits: Some benefits provided to employees continue to be tax-free for the employee, but will be treated as UBI for the tax-exempt employer effective January 1, 2018. These provisions were covered in the first article of this series, which can be found here: http://www.leadingageca.org/tax-reform-part1

Tax rates: The corporate tax rate was changed to a flat 21 percent for incorporated organizations; the previous corporate rates ranged from 15 percent to 35 percent. Trusts tax brackets were adjusted and reduced – rates prior to 2018 ranged from 15 percent to 39.6 prcent; beginning January 1, 2018, trust rates range from 10 percent to 37 percent. Fiscal year filers will use a blended tax rate for the year that spans December 31, 2017.

Separate activity calculation: the law requires organizations that carry on more than one unrelated business activity to separately calculate taxable income for each activity. This would effectively prohibit using deductions relating to one unrelated business activity from offsetting the taxable income of another unrelated business activity. For example, if an organization has a net profit from providing management services to unrelated organizations, and has a net loss from rental activities that are unrelated to their tax exempt purpose, the net loss from the rental activity cannot be used to offset the net profit from the management services when Form 990-T is filed. Instead, the loss from the rental activity will be carried forward to offset future rental income.

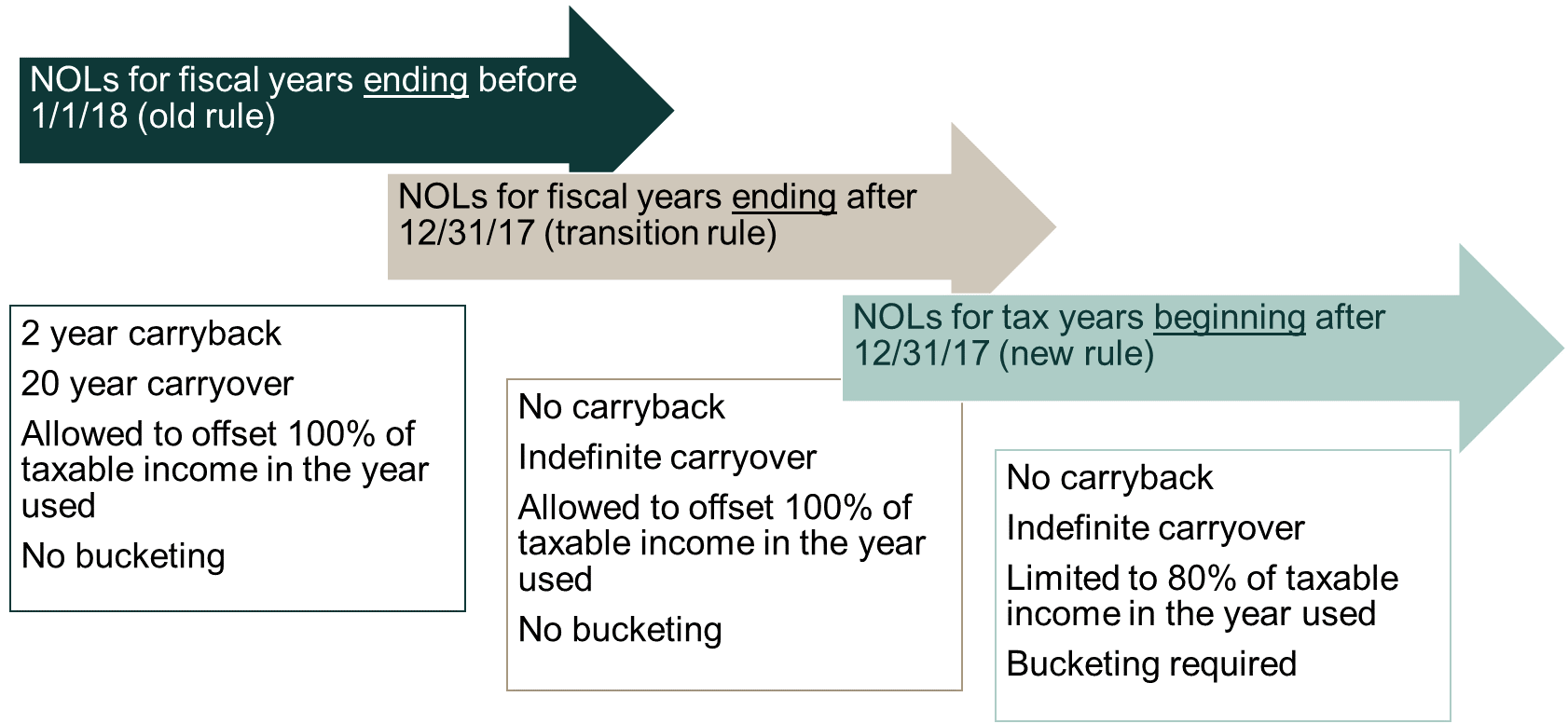

Net operating losses (NOLs): losses from taxable income are now split into two or three layers, depending on if the organization files a calendar year of a fiscal year return:

• NOLs generated in years ending before January 1, 2018 are subject to the old rules and are generally allowed to be carried back for two years and forward for 20 years. The loss can offset any taxable income on Form 990-T at 100 percent.

• NOLs generated in a fiscal year ending after December 31, 2017 cannot be carried back, can be carried forward indefinitely, and are allowed to offset any taxable income on Form 990-T at 100%. This layer does not apply for calendar year filers as it’s a transition year rule only.

• NOLs generated in years beginning after December 31, 2017 cannot be carried back, and can be carried forward indefinitely. However, the loss can only offset up to 80% of taxable income in the year used, and can only offset income from the activity generating the loss.

Alternative minimum tax: the law repeals the corporate alternative minimum tax (AMT) and allows the AMT credit to offset regular tax liability for any taxable year. The AMT credit may be refundable in tax years beginning after 2017 and before 2022, subject to certain provisions. AMT was not repealed for trusts.

Credit for paid leave: a new general business credit is available for calendar years 2018 and 2019 for wages paid to qualifying employees who are on family and medical leave. The credit ranges from 12.5 percent to 25 percent of wages paid for between two and 12 weeks of leave, and can be claimed against unrelated business income tax on Form 990-T, or on Form 1120 for a taxable corporation.

For more information about these changes and other tax reform provisions, visit our website at www.mossadams.com/tax-reform and https://mossadams.com/articles/2017/december/how-tax-reform-could-impact-not-for-profits